Markets are entering a new era defined by macroeconomic tension, evolving portfolio preferences and shifting leadership across asset classes. Mounting global public debt, multi‑decade highs in long‑term bond yields and trade‑policy volatility are prompting investors—and central banks—to recalibrate traditional allocation models.

In this environment, we observed increased interest in U.S. large‑caps buoyed by AI-driven growth, gold’s seasonal demand as a potential hedge, and a growing rush into income opportunities, including covered‑call ETFs. This analysis explores those dynamics and their potential impact as we navigate the second half of 2025.

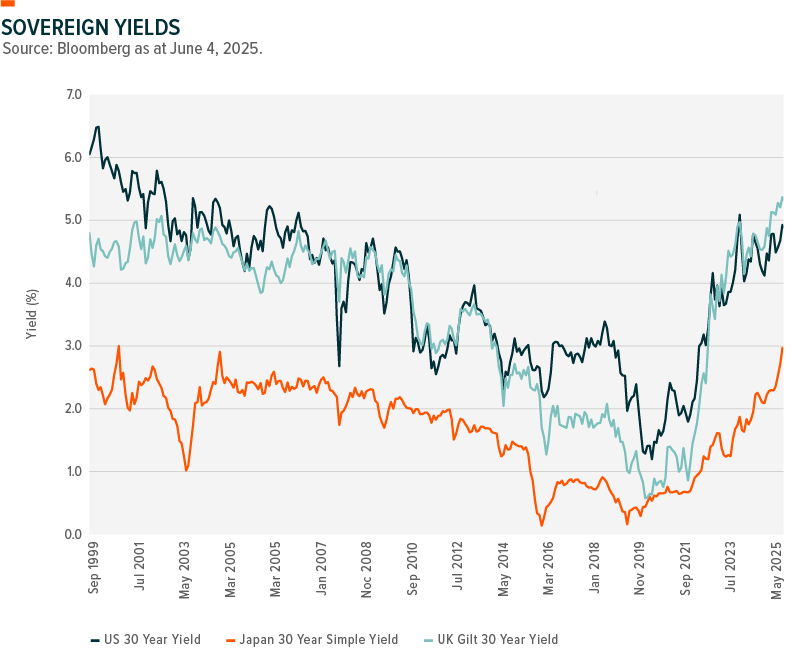

Global Debt Pressures Continue to Build

- Rising global public debt is an emerging concern, with the International Monetary Fund (IMF) projecting it will surpass 95% of global Gross Domestic Product (GDP) by 2025, and potentially hit 100% by 2030. Slowing economic growth, persistent deficits, and the broader effects of deglobalization are placing mounting pressure on sovereign balance sheets, with implications for long-term market stability and investor confidence.

- Long-term bond yields have surged to multi-decade highs across major developed markets, underscoring rising risk premiums and investor uncertainty. Japanese 30-year government bonds recently hit an all-time high of 3.1%, U.K. gilts climbed above 5.3% for the first time since the 1990s, and U.S. 30-year Treasuries breached 5% levels not seen since before the global financial crisis.

- Navigating rising debt levels alongside trade policy volatility will demand greater agility from central banks. With tariffs and fiscal strain converging, policymakers face growing challenges in balancing inflation targets with financial stability mandates, which could prompt more complex monetary and geopolitical discussions throughout the remainder of the year.

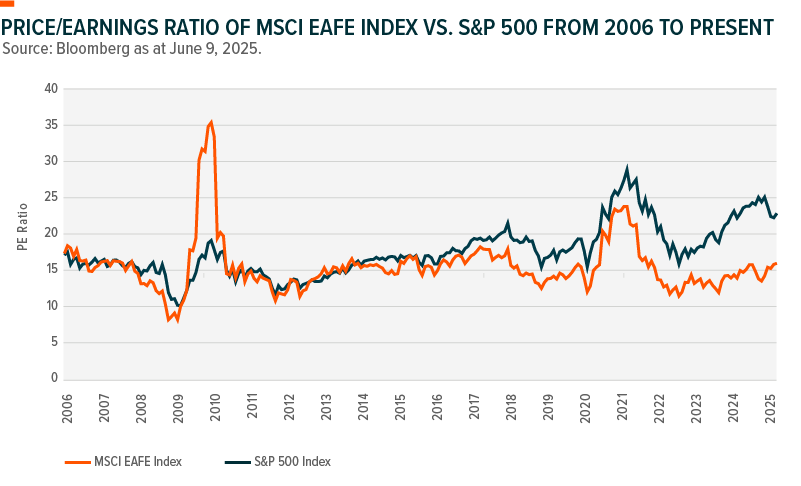

Don’t Write-Off U.S. Markets

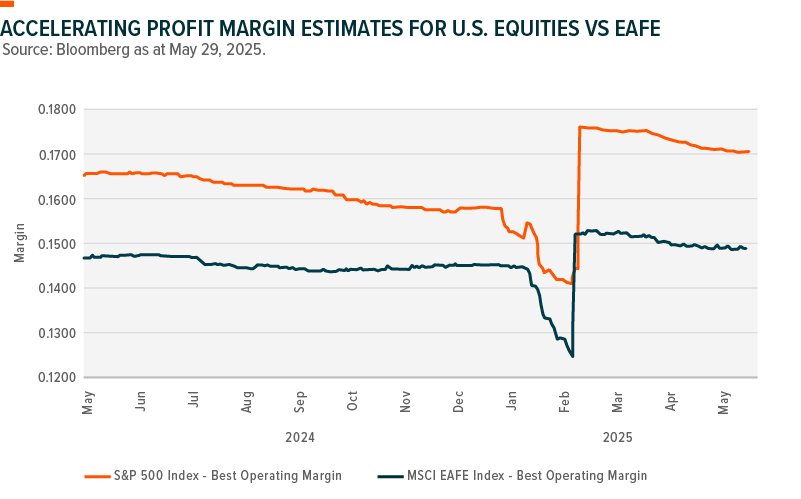

- U.S. equities remain in favour, with earnings growth expected to outpace international peers over the next 12 months. Stronger secular trends, superior earnings visibility, and the high-quality nature of U.S. large-caps companies—particularly in the technology sector—continue to support investor confidence. Even with elevated valuations, the relative strength of fundamentals could sustain U.S. market leadership in the absence of major positive surprises from Europe or Japan.

- While the Europe, Australia and the Far East (EAFE) equities have narrowed the gap due to a cyclical rebound, attractive valuations, and supportive central bank policy, this suggests that some of the recent gains may already reflect anticipated improvements. A shift in U.S. Federal Reserve (Fed) rhetoric, particularly a clearer path to rate cuts, could reignite capital flows back into U.S. markets, especially if global economic surprises fail to meet expectations or if the dollar remains strong.

- Key risks to U.S. markets include labour market deterioration, possible earnings downgrades from late-2025 tariff disruptions, and bond yields drifting persistently toward 5%. However, a more dovish Fed stance and a modestly weaker dollar could cushion these pressures. AI-driven growth, especially among mega-cap tech names like the “Magnificent 7,” may continue to provide a powerful offset, should policy easing arrive on schedule.

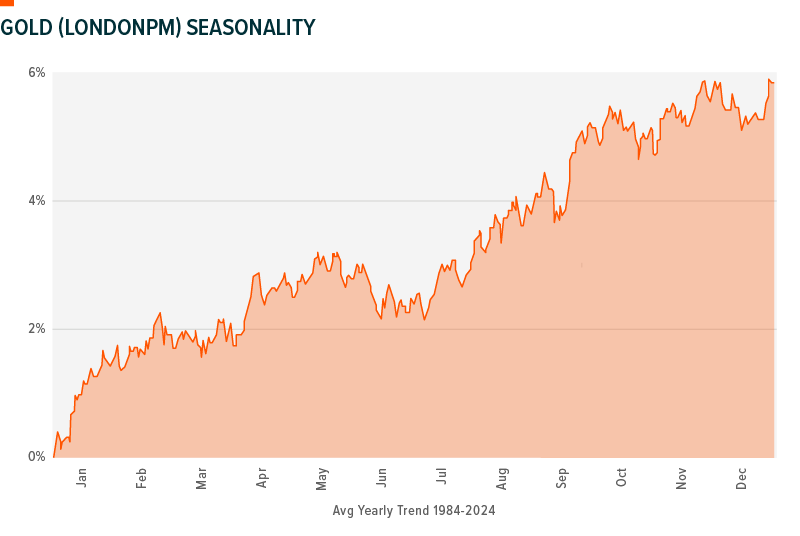

Gold Outperforms During Key Seasonal Windows

- Gold typically enters a strong seasonal period starting in July, though the setup often begins in June. Historically, June tends to mark a low point in price, followed by a multi-month rally. Volatility in June has often created compelling entry points for investors positioning ahead of gold’s seasonal strength, particularly when broader market sentiment is uncertain.

- June is often a volatile month for gold, but this turbulence has frequently led to longer-term gains. Gold tends to bottom in June before rising steadily, a pattern that has repeated across multiple years. Given heightened volatility and global macro headwinds, June may again offer a window of opportunity ahead of the typical July–September upswing.

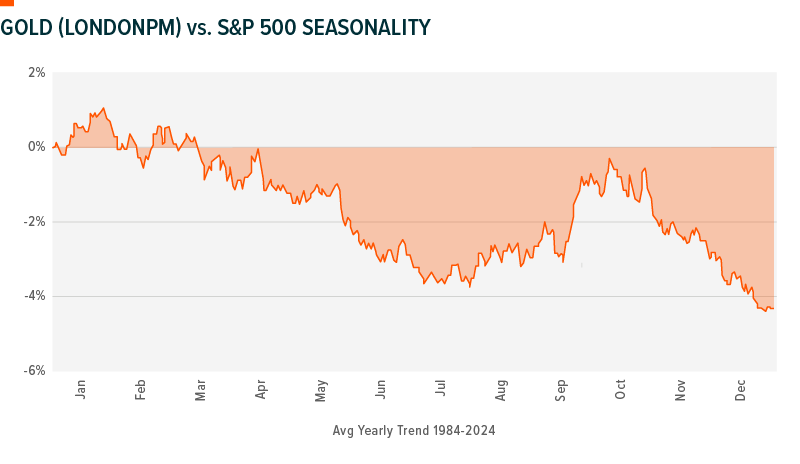

- Despite trading near record highs, gold has outperformed the S&P 500 during recent seasonal rallies, with gains of 13% in 2023 and 27% in 2024. As the seasonal tailwind re-emerges and gold continues to serve as a hedge against volatility, inflation, and geopolitical risk, the current setup could support renewed momentum in both bullion and miners.

Source: AlphaMountain.com

Caution Rises, Rotation Risk Increases Globally

- I’m closely watching how tariff-driven uncertainty could challenge the narrative of U.S. exceptionalism and weigh on the U.S. dollar. Since Liberation Day, investor sentiment toward U.S. assets has shifted, with relative valuations compressing compared to EAFE and emerging markets. This shift may mark a turning point in capital allocation patterns.

- Investor caution is also reflected in slower capital flows into U.S. markets and a more deliberate approach to managing currency exposure. Hedging against the U.S. dollar has increased compared to pre-Liberation Day levels, suggesting growing concern around the currency’s medium- to long-term trajectory, even as it remains a default safe haven.

- This environment may support a relative rotation toward EAFE and emerging markets, particularly those with more compelling currency dynamics and valuation appeal. As flows seek opportunity beyond the U.S., the second half of 2025 could see broader international participation, provided macro conditions and sentiment remain supportive.

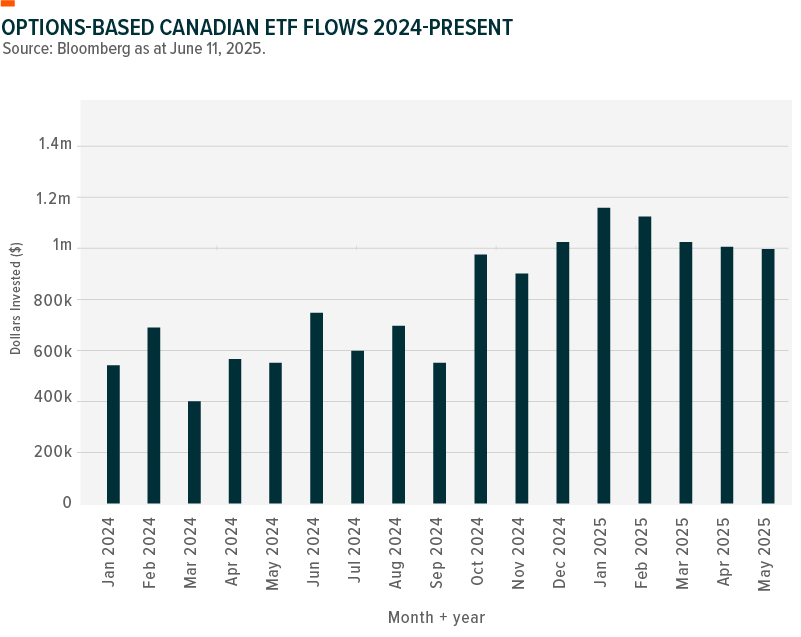

Options ETFs Grow as Yields Matter

- Covered call and options-based exchange traded funds (ETFs) are capturing a growing share of investor interest in Canada, with nearly 10% of net inflows now directed toward these strategies. This upward trend has gained momentum through late 2024 and into 2025, supported by a steady stream of new offerings and Canadians’ continued demand for yield-focused investment vehicles.

- Options-based strategies have become a favoured tool for navigating market volatility, offering the dual benefit of income generation and downside cushion. Covered call structures allow investors to stay fully invested while collecting option premiums—often elevated during turbulent periods— which may help mitigate risk and enhance overall yield depending on market conditions.

- The options ETF landscape is evolving rapidly, extending beyond traditional equity buy-write approaches. Investors can now access strategies built around fixed income exposure, varying levels of duration, lightly leveraged enhancements, and even niche segments like Bitcoin covered calls, broadening the opportunity set across asset classes and market cycles.

With monetary policy uncertainty set to persist, market participants should remain nimble and diversified. U.S. equities may continue to benefit from earnings resilience and innovation leadership, while selective exposure to international markets makes sense if currency and valuation trends shift. Gold and covered call strategies remain compelling diversification plays amid volatility, and rising yields will test debt sustainability, accentuating the need for a flexible, multi‑asset approach.

Investors who thoughtfully blend growth, income and defensive elements could be best positioned to navigate opportunities in a more complex global investment environment.