By Global X Research Team

Key Takeaways

- Semiconductors power the digital economy, enabling technologies from AI to smartphones. Invented in the U.S., they remain a national strength, with American firms accounting for nearly half of global chip sales.

- President Trump’s “Big Beautiful Bill” offers 35% tax credits to boost U.S. chip manufacturing, encouraging companies to invest billions in new plants. While the U.S. pioneered semiconductors, manufacturing is dominated by Taiwan and South Korea. China’s ambitions remain limited by U.S. export controls and tariffs.

- The semiconductor sector is recovering broadly, with 2025 sales projected to rise 11–14%, driven by memory and logic chips, AI demand, and normalized inventories supporting steadier pricing and renewed capital spending plans.

Computer chips are powering the digital economy but it’s the small and mighty semiconductors within these chips that make it all possible. From enabling technologies like generative Artificial Intelligence (AI), to expanding the growth of the power grid with nuclear power and electrical utilities, that the semiconductor industry is a key input transforming industries and our future.

Since the transistor’s invention 70 years ago, semiconductors have driven advancements from personal computing and smartphones to data centres and cloud services.

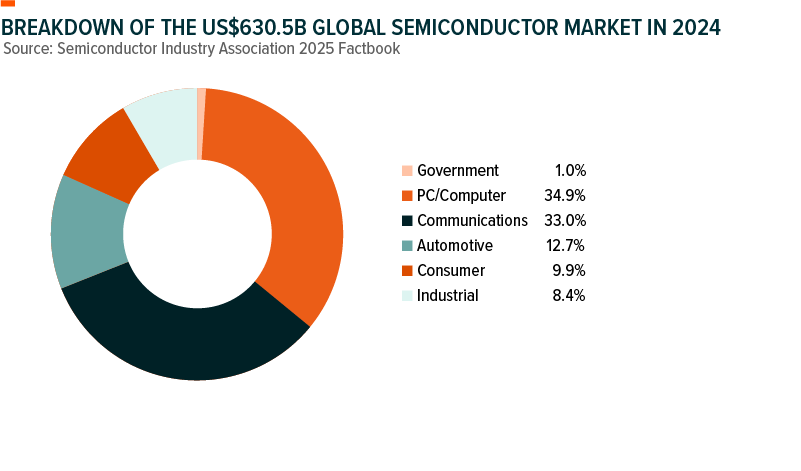

They underpin systems we use to work, communicate, travel, entertain, harness energy and make scientific discoveries. Invented in America, semiconductors remain a U.S. strength, with American companies still leading the global market and accounting for nearly half of the world’s chip sales.1 You can find a full introduction to the industry here.

Trump’s “BBB” to Boost American Chip Capabilities

While the U.S. pioneered semiconductor technology, manufacturing is now dominated by Taiwan and South Korea. China remains the largest consumer of semiconductors and is pushing to produce more domestically, but U.S. export controls and tariffs continue to limit China’s progress on advanced chip production.

The Trump administration has shifted away from Biden’s incentive-based approach to boosting U.S. chip manufacturing. While the CHIPS and Science Act used subsidies to lower domestic production costs, Trump’s strategy focuses on tariffs to penalize overseas sites, encouraging companies to build locally.

To help boost U.S. efforts to onshore chip production, President Trump’s “Big Beautiful Bill” makes it cheaper for chip companies to build plants on American soil. Companies such as Intel, Taiwan Semiconductor Manufacturing Co. (TSMC) and Micron Technology will be eligible for an investment tax credit of 35% if they begin construction on new chip plants before 2026.

Additionally, leading American chip manufacturers have announced significant investment plans to reshore chip production capabilities: Texas Instruments (TI), the oldest company in the chip industry, will invest more than $60 billion across seven U.S. semiconductor plants, which will support more than 60,000 jobs. Peers such as Micron Technology and GlobalFoundries have also announced spending plans for new American chip plants.

These measures aim to strengthen U.S. semiconductor manufacturing, supporting both economic growth and national security.

Sector Recovery

The semiconductor sector has gone through several phases in recent years, which include Pandemic-linked supply shortages followed by a slower period from adjusted inventories and more selective capital spending.2

These days, the sector appears to be thriving: for the first quarter of 2025, global semiconductor sales rose 18.8% year-over-year to $167.7 billion. And major chip firm Broadcom is forecasting third-quarter revenue above analyst estimates thanks to strong demand for its computing chips. Broadcom’s chips are designed for AI and cloud computing companies such as OpenAI and Google.

The industry outlook also looks promising: according to the World Semiconductor Trade Statistics (WSTS) organization, the semiconductor market is expected to grow 11.2% in 2025 to US$697 billion. This growth is primarily driven by the memory and logic chip segments. A forecast from specialist research firm Gartner is even more bullish, projecting 14% growth in 2025 to reach US$717 billion. The research firm attributes this growth to the continued surge in AI-related semiconductor demand and recovery in electronic production.

AI continues to be a major structural driver for semiconductors, but it is not the main reason the sector is seeing improvement right now. The recovery underway is broader and more linked to supply discipline, inventory normalization, and steady demand across traditional end markets, including the broader growth of digital and electrical infrastructure.3

Don’t Forget About Memory Chips

Memory chips – divided into dynamic random access memory (DRAM) chips, which manage data and require power and “not and” (NAND) chips, which store data but don’t need power – are a significant influence on the overall semiconductor market. These chips can be found in smartphones, PCs and servers.

DRAM and NAND chips are seeing more stable pricing as customers return with greater confidence.4 This is not due to a sudden demand spike but because production was cut early, and inventories have now cleared through the system. The result is a more balanced environment where pricing can reset gradually without distorting fundamentals.

A similar pattern is emerging across equipment, testing, and packaging firms, which tend to lead the cycle given their exposure to early-stage production and planning. Stronger pipelines here suggest that manufacturers are preparing for sustained output rather than reacting to one-off orders.5

The common thread across all of this is breadth. It is not a one-theme rally or a single-product move. Demand is re-emerging across multiple industries and production layers, which makes the recovery more durable and more investable.6

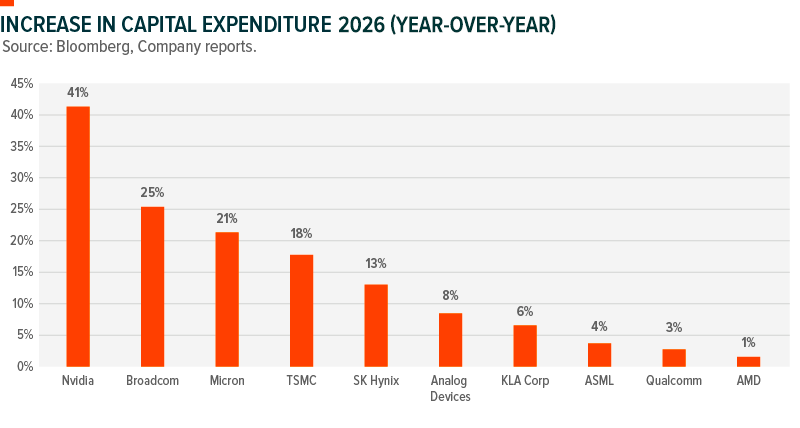

Capital Spending and Order Patterns Are Starting to Matter Again

One of the more notable shifts in recent months has been the return of more structured capital spending plans from key customers. Throughout 2023, many firms took a cautious approach to new orders and deferred expansion. That is starting to change. Foundries are confirming new customer allocations. Equipment makers are seeing higher utilization as inventory levels normalize, customer forecasts firm up, and confidence returns to capital spending plans across foundries and packaging. Packaging capacity is being booked out earlier, with clients signalling firm delivery windows.7

Why This Matters Now

The recovery unfolding in semiconductors is being supported by tangible shifts in how companies manage production, allocate capital, and respond to more consistent demand signals. Activity is broadening across memory, analog, logic, and equipment, with many companies now reporting clearer visibility and steadier margin progression.

These improvements follow a period of adjustment, where inventories were drawn down, supply chains stabilized, and capital spending became more deliberate. That reset is starting to show through in order patterns and operational performance.

How to Invest

For Canadian investors interested in investing in the semiconductor sector, they can consider individual stocks of chipmakers or a semiconductor-themed investment vehicle such as an exchange-traded fund (ETF), which offers a diversified selection of stocks with a simple fee structure.

The Global X Artificial Intelligence Semiconductor Index ETF (CHPS) offers exposure to some of the largest global companies that design, manufacture, and distribute semiconductors as well as companies engaged in the AI semiconductor value chain, while the Global X Big Data & Hardware Index ETF (HBGD) provides exposure to global companies directly involved in data development, storage, and management-related services, as well as hardware.

Related ETFs

CHPS – Global X Artificial Intelligence Semiconductor Index ETF

HBGD – Global X Big Data & Hardware Index ETF

Footnotes

1 Semiconductor Industry Association 2025 Factbook.

2 Global X Australia as at June 4, 2025, Back in the Saddle: Semiconductor Sector Turning and Repricing.

3 TrendForce as at March 26, 2025, NAND Flash Prices Begin to Recover in 2Q25 as Production Cuts and Inventory Rebuilding Take Effect

4 PatentPC as at May 6, 2025, Memory Chip Market in 2024: DRAM & NAND Pricing, Demand, and Future Trends

5 Semi.org as at April 9, 2025, Global Semiconductor Equipment Billings Surged to $117 Billion in 2024

6 Reuters as at November 26, 2024, Analog Devices Beats Q4 Targets On Chip Demand Recovery from Auto Industry

7 S&P Global as at July 23, 2024, Semiconductor Supply Chain Q3 2024 Outlook: Multispeed Recovery

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

For more information on Global X Investments Canada Inc. and its suite of ETFs, visit www.GlobalX.ca

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2025 Global X Investments Canada Inc. All Rights Reserved.

Published July 17, 2025.

How Canadian Investors Use Finfluencers to Learn About Investing

Not ready to invest, but curious to learn more?

Subscribe for research perspectives, market commentary, and charts of the trends shaping global markets. We promise not to overwhelm you – updates will be periodic and timely.