Key Takeaways

- After a post-Fukushima downturn, uranium is back in focus as nuclear power is increasingly seen as a solution for rising electricity demand, energy security and lower-emissions generation. As reactor restarts and nuclear capacity growth continue, the outlook for uranium has improved alongside the outlook for nuclear itself.

- Momentum is building across the nuclear industry through reactor construction, restarts, uranium supply agreements, enrichment investment and support for small modular reactors (SMRs). Activity in Canada, the U.S., China, India, the U.K. and Kazakhstan reflects a broader global push to expand nuclear capacity.

- AI and data-centre growth are lifting long-term electricity demand expectations, while uranium supply faces constraints from mine depletion, long lead times and shrinking secondary supply. That backdrop is increasing attention on opportunities across the nuclear value chain, from uranium miners to reactor and component manufacturers.

Uranium has moved back into focus as improving nuclear sentiment, rising policy support, and growing electricity demand reshape the outlook. This piece looks at the nuclear comeback, industry momentum across key markets, the role of AI and data centres in power demand, tightening uranium supply, and where opportunities may emerge across the nuclear value chain.

Uranium Returns to the Spotlight

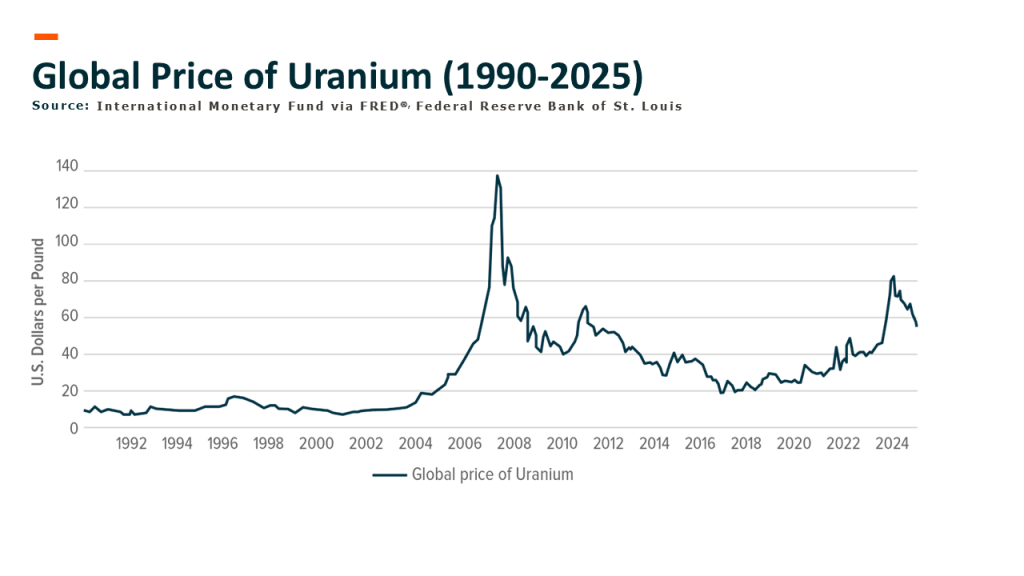

The uranium market has always been cyclical, but few commodities are as sensitive to public policy and investor sentiment. After the Fukushima disaster in 2011, nuclear development slowed sharply, uranium prices fell, and producers shut mines as demand expectations weakened.

The slump in uranium market prices from 2011 to 2021, coupled with uncertainty around nuclear power development in some countries, led to reduced uranium demand, depressed prices, and a slowdown in mine production and development.

“The rally in the price of uranium that we have seen recently, from 2021, although it has been a strong rally, pales in comparison to the rally from 2002 to 2007. From this perspective, we are still in the early stages of the uranium rally, which could potentially go much higher,” says Global X Research Analyst Brooke Thackray.

“The problem with the decline of uranium prices is that it made uranium mining companies pull back on expansion plans. Prices can correct higher in the short-term, as they have done recently, but planning and building a greenfield uranium mine can take ten to fifteen years.”

It isn’t just resource sites that take a long time to develop: it takes a decade or more to actually build a nuclear power plant. However, with nuclear power increasingly viewed as part of the solution to rising power demand, energy security concerns and lower-emissions generation, the outlook for uranium has started to improve alongside the outlook for nuclear itself.

Nuclear comeback

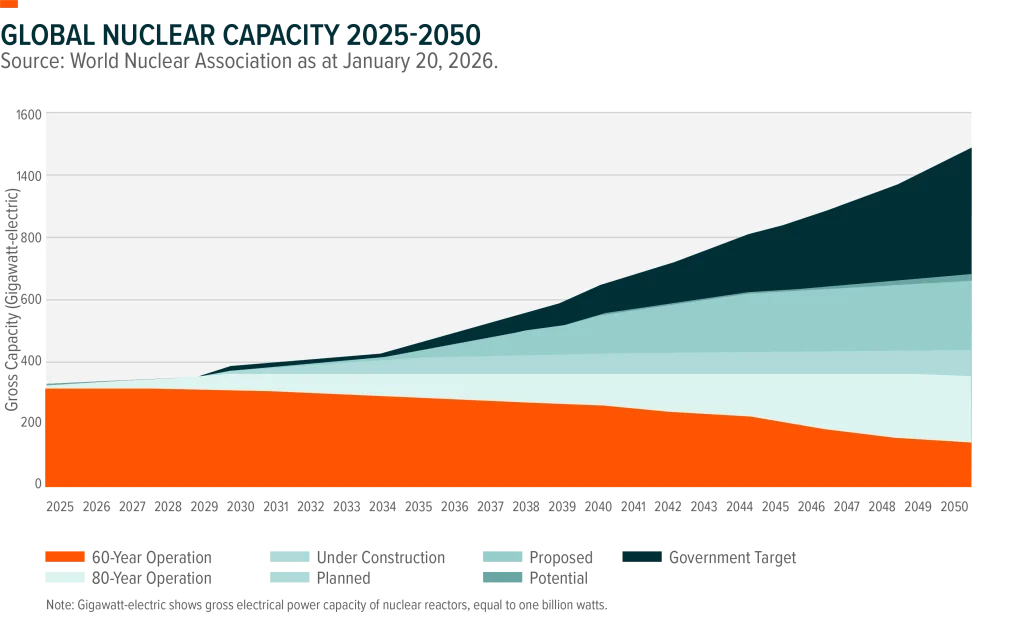

Global nuclear power output reached a record in 2025 and is expected to continue rising through 2050 as governments and companies seek to meet growing demand for reliable electricity. More than 40 countries now include nuclear energy in their strategies and are taking steps to develop new projects.

Investment is also rising across both traditional large-scale plants and newer technologies such as SMRs. In addition to reactor restarts, particularly in Japan, more than 70 gigawatts of new nuclear capacity are under construction, one of the highest levels seen in 30 years, while Microsoft and Constellation Energy in the U.S. plan to restart a mothballed nuclear plant at Pennsylvania’s Three Mile Island.

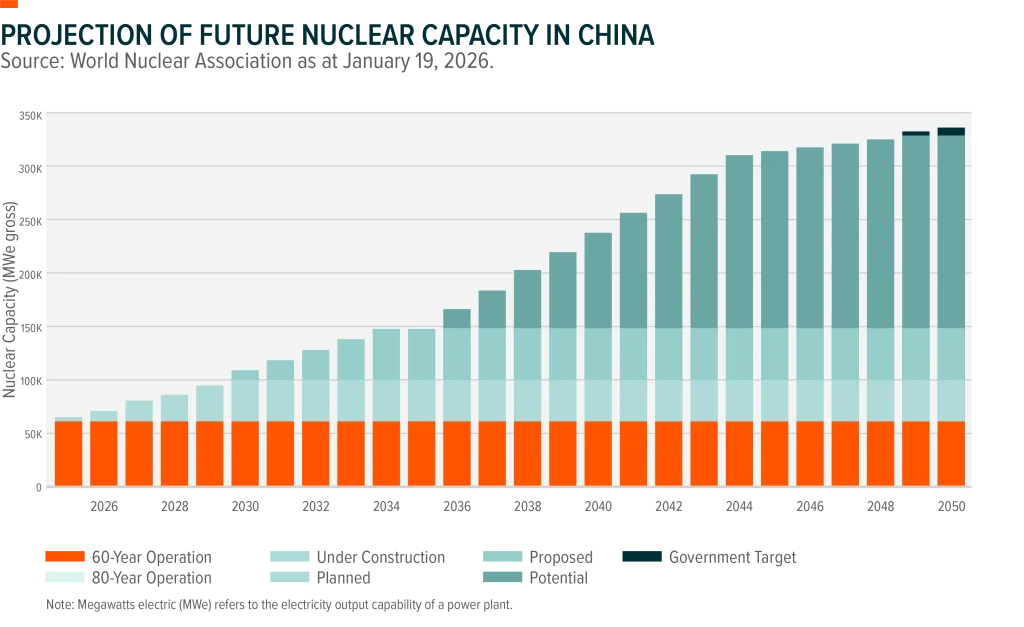

China is leading much of the buildout in net-new nuclear capacity. According to data from the World Nuclear Association, China is building 46% of the world’s nuclear power plants that are currently under construction, making it the country developing nuclear power at the fastest rate and is on track to become the world’s largest nuclear power operator by around 2030.

Including these and other developments, global nuclear power capacity is projected to increase by at least one-third by 2035.

Industry Momentum

Saskatoon-based Cameco signed a $2.6 billion deal with India to supply 22 million pounds of uranium over nine years to help fuel the country’s 24 nuclear reactors.

Cameco sources its uranium from two mines in northern Saskatchewan: Cigar Lake and McArthur River/Key Lake.

Denison Mines Corp. is also moving ahead with the construction of a proposed uranium mine in northern Saskatchewan, which could potentially be the first uranium mine to be built in Canada in a generation.

In the United States, recent policy developments are also helping revive the industry after nearly three decades of limited construction.

As part of efforts to restart domestic production and reduce reliance on Russian supplies, the U.S. moved ahead with establishing at least two more domestic nuclear fuel enrichment facilities. The U.S. was a leading uranium producer from the 1960’s to the 1980’s.

Russia supplies over 40% of global uranium enrichment services and 20-30% of the enriched nuclear fuel used in the U.S. and Europe.

NVIDIA and the Idaho National Laboratory have entered into a partnership to advance nuclear research and development using Artificial Intelligence (AI), while California is reconsidering its ban on nuclear power expansion.

META agreed to unlock a combined 6.6 gigawatts of nuclear power with providers, while the Province of Ontario agreed to share SMR technology with the State of New York.

Elsewhere, the U.S. Department of Energy awarded $2.7 billion in task orders to expand domestic uranium enrichment capacity and announced $800 million in grants to support the development of SMRs.

Internationally, momentum has continued to build as well. Kazatomprom, the world’s largest uranium producer, signed an agreement to sell a significant portion of its supply to India.

The U.K. government is overhauling nuclear regulation to speed up projects. The nation relies on natural gas for one-third of its energy and the volatility in energy markets following the Iran conflict has highlighted the U.K.’s exposure to geopolitical shocks and global energy price swings.

“In the last few years, the U.K. government has committed to greater amounts of energy sourced from nuclear power as nuclear power has been classified as a source of “green” energy,” Thackray adds.

AI And Data Centres Drive Demand

Part of the renewed interest in nuclear power comes down to two broad forces: energy security and rising electricity demand.

Energy security has moved back up the political agenda, and nuclear power offers a source of low-emissions baseload electricity that can support a more secure and diversified electricity mix.

At the same time, AI-driven infrastructure growth is adding to expectations that power demand could remain elevated for decades.

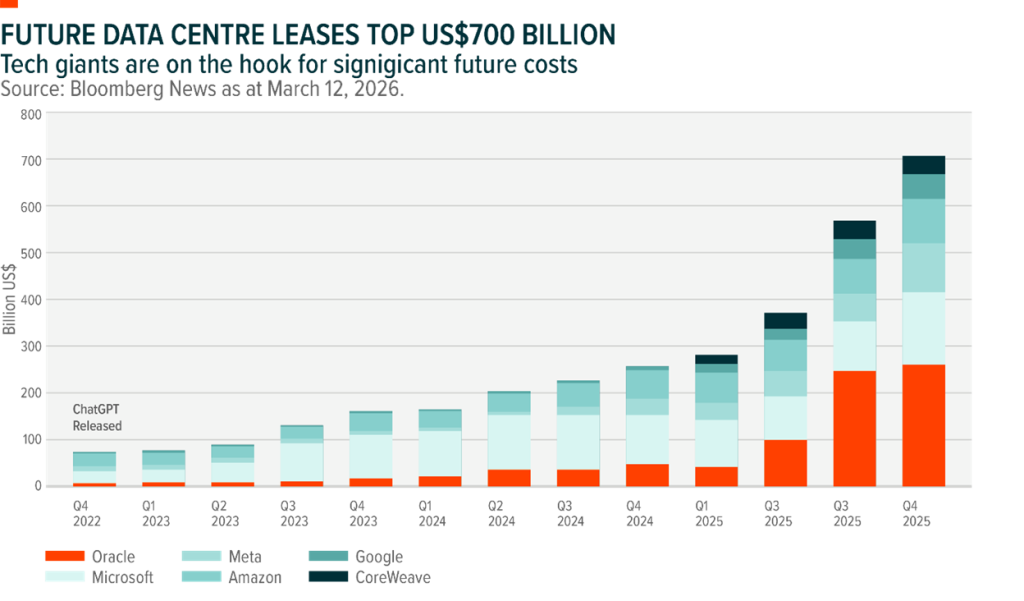

Moody’s Ratings estimates that at least US$3 trillion will flow into data centre-related investments over the next five years. Major U.S. technology firms including Microsoft, Amazon, Alphabet, Oracle, Meta Platforms and CoreWeave invested U$700 billion on data centres in the fourth quarter of 2025.

“As AI has ramped up over the last few years, demand for electricity has also ramped up, putting greater strain on the electrical grid. Nuclear power is being seen as a significant base load provider of electricity in the future to power AI.”

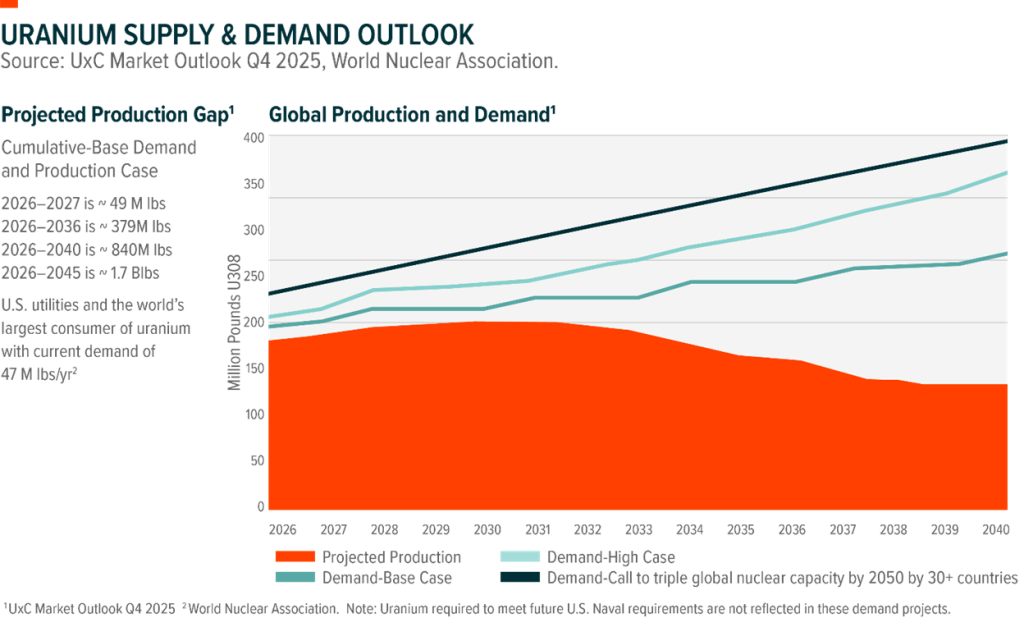

Supply Situation

The deficit between mined uranium and global reactor demand is expected to grow. Output from today’s mines is expected to halve between 2030 and 2040 as existing mines are depleted. Kazakhstan currently holds the title of world’s leading supplier of uranium, supplying 40% of the world’s uranium needs in 2025.

The U.S. Nuclear Energy Agency estimates that if demand for nuclear energy grows, current uranium deposits will be depleted by 2080.

Meanwhile, deficits are expected to rise, hampered by long lead times on new mines and shrinking secondary supply, just as a new wave of reactor-driven uranium demand is expected to hit the grid.

Value chain opportunity

This opportunity spans the entire nuclear value chain, from miners and uranium suppliers to advanced reactor developers and industrial companies producing reactor components.

Ways to Gain Exposure

For investors looking to gain exposure to this theme, there are different ways to approach it depending on where they see the potential opportunity.

The Global X Uranium Index ETF (HURA) provides exposure to companies that are primarily involved in the uranium mining and exploration industry and to the price of the underlying commodity.

HURA seeks to replicate, to the extent possible, the performance of the Solactive Global Uranium Pure-Play Index. This index is designed to provide exposure to the performance of a group of global exchange-listed companies involved in uranium mining and exploration or in some cases, invest and participate directly in the physical price of uranium.

Additionally, the Global X Artificial Intelligence Infrastructure Index ETF (MTRX) provides exposure to companies involved in AI infrastructure, diversifying exposure to electric utilities, data center equipment manufacturing, and energy commodities like uranium and copper, aligned with themes related to long-term growth in AI’s backbone.

Taken together, these developments suggest nuclear power is moving back into the global energy conversation. Rising electricity demand, stronger policy support and renewed investment across the nuclear value chain are contributing to renewed attention on both nuclear power and uranium.

Related ETFs

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain ETFs are alternative investment funds (“Alternative ETFs”) within the meaning of the National Instrument 81-102 Investment Funds (“NI 81-102”) and are permitted to use strategies generally prohibited by conventional mutual funds, such as the ability to invest more than 10% of their net asset value in securities of a single issuer, the ability to borrow cash, to short sell beyond the limits prescribed for conventional mutual funds and to employ leverage of up to 300% of net asset value. While these strategies will only be used in accordance with the investment objectives and strategies of the Alternative ETFs, during certain market conditions they may accelerate the risk that an investment in ETF Shares of such Alternative ETF decreases in value. The Alternative ETFs will comply with all requirements of NI 81-102, as such requirements may be modified by exemptive relief obtained on behalf of the ETF.

The financial instrument is not sponsored, promoted, sold, or supported in any other manner by Solactive AG nor does Solactive AG offer any express or implicit guarantee or assurance either with regard to the results of using the Index and/or Index trade name or the Index Price at any time or in any other respect. The Index is calculated and published by Solactive AG. Solactive AG uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the Issuer, Solactive AG has no obligation to point out errors in the Index to third parties, including but not limited to investors and/or financial intermediaries of the financial instrument. Neither publication of the Index by Solactive AG nor the licensing of the Index or Index trade name for use in connection with the financial instrument constitutes a recommendation by Solactive AG to invest capital in said financial instrument nor does it in any way represent an assurance or opinion of Solactive AG with regard to any investment in this financial instrument.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

For more information on Global X Investments Canada Inc. and its suite of ETFs, visit www.GlobalX.ca

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2026 Global X Investments Canada Inc. All Rights Reserved.

Published April 10, 2026.

How Canadian Investors Use Finfluencers to Learn About Investing

Not ready to invest, but curious to learn more?

Subscribe for research perspectives, market commentary, and charts of the trends shaping global markets. We promise not to overwhelm you – updates will be periodic and timely.