Key Takeaways

- The U.S. Federal Reserve (Fed) and Bank of Canada (BoC) are due to unveil rate decisions on September 17 amid cooling inflation, slower hiring, and signs of stagnating economic growth on both sides of the border.

- Markets expect both the BoC and Fed to ease rates, as soft inflation, gross domestic product (GDP), and labour data in Canada and weakening U.S. jobs data, build the case for near-term monetary policy shifts.

- Global X’s Premium Yield ETFs blend bond income with options overlays, offering high yield potential, downside protection, and reduced volatility. These ETFs help capture potential yield curve opportunities, offering consistent income and diversification amid an easing rate cycle.

As investors gear up for the last quarter of the year, attention is turning to a critical date: September 17, when both the Fed and BoC deliver rate decisions that could reshape the market landscape, while taking into account a complex macroeconomic environment. For bond investors, yield curve shifts, interest rate expectations, and central bank guidance are back in the spotlight which offers both challenges and potential opportunities across government bond markets.

A Fragile Macro Moment

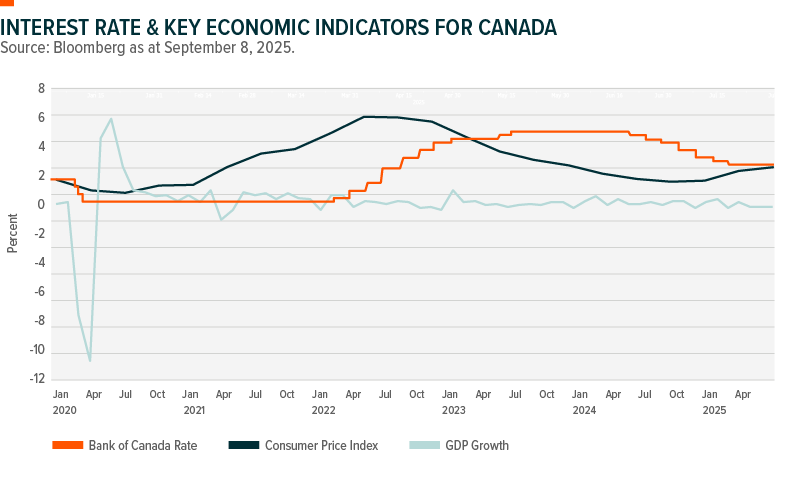

Canada’s economy is treading carefully. The Bank of Canada held its key rate steady at 2.75% in July, as inflation fell to 1.7% in July from 1.9% a month earlier and GDP showed signs of stagnation. Labour market softness may have added to the case for easing.

South of the border, the data is softening. The August jobs report showed just 22,000 jobs added and an uptick in the unemployment rate to 4.3%. Additionally, separate data showed there were more unemployed people than positions available for the first time since the COVID-19 pandemic, while revised data suggests that the U.S. jobs market may be weaker than previously thought.

In its most recent reading of the economy, the Fed said there was “little or no change” in economic activity across the United States. At the same time, inflation appears to be cooling as the latest numbers showed consumer prices in August rising in line with market expectations, prompting investors to reprice expectations for the Federal Reserve. However, with President Trump’s global tariff policy, the threat of stagflation is still on the minds of investors.

“Recent trends in U.S. economic data suggest a difficult path ahead for the Fed, as there could be diverging risks to their dual mandate,” says Jean-Christian Daigle, Vice President and Portfolio Manager, Option Overlays at Global X.

“The labour market cracks are more apparent – with year-to-date revisions reaching roughly one million, while the US Administration’s trade war could jeopardize the progress made so far on lowering inflation, which has proven to be stickier than expected.”

These policy shifts are unfolding against a backdrop of diverging growth trajectories. The OECD downgraded global GDP forecasts to 2.9% for both 2025 and 2026, while the organisation projects the U.S. to slow from 2.8% growth in 2024 to 1.6% this year. Canada’s numbers are similarly tepid, weighed down by weak housing data and external trade demand.

Ahead of the (yield) curve

Rate decisions also affect bond yields, which simply put, are the return on the capital invested. Yields rise as interest rates climb and fall when they are cut. Bond prices and yields also move in opposite directions: falling prices boost yields and rising prices lower them.

Central banks adjust interest rates to manage inflation and support economic growth. Higher inflation often pushes bond yields higher and bond prices lower.

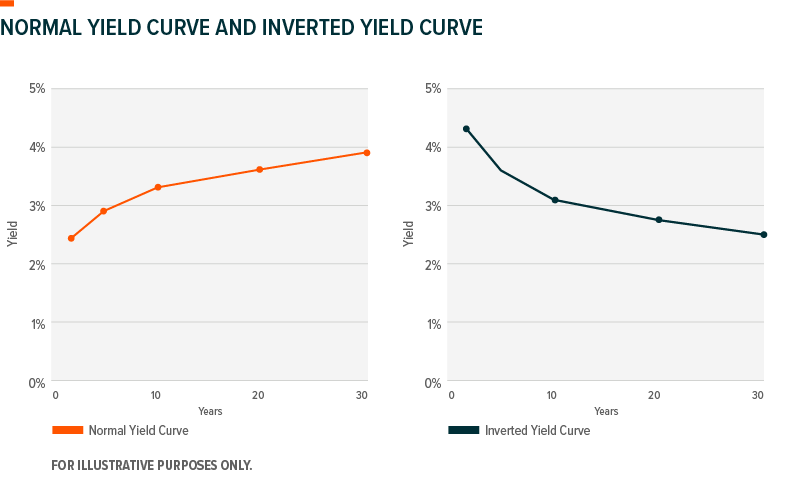

Investors typically demand higher yields for longer-term bonds due to uncertainty about future conditions which results in an upward-sloping, or “normal,” yield curve. However, when yields on shorter-term bonds exceed those of longer-term ones, the curve inverts.

Yield curves show interest rates across bond maturities from three months to 30 years or more. While a normal curve suggests optimism, an inverted curve signals caution about the near-term outlook—typically tied to expectations for declining rates or weaker growth.

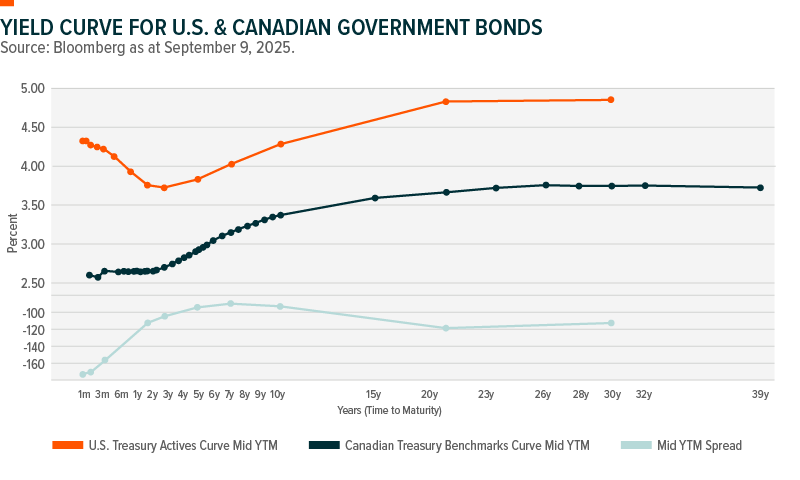

Here’s the yield curve for U.S. and Canadian government bonds:

An inverted yield curve is often viewed as a leading indicator of recession. It reflects market sentiment that economic growth will slow—and that central banks may need to respond by cutting rates.

This dynamic tends to increase demand for long-term bonds, pushing their prices up and yields down. Historically, yield curve inversions have preceded downturns, though distortions following the COVID-19 pandemic have reduced the reliability of this signal.

What Investors Should Watch

Whether rate paths diverge or converge, here are four key metrics and trends investors should keep in mind:

- Shifting Yield Curve Dynamics: Watch for steepening at the front of the yield curve around short durations.

- Cross-Border Rate Differentials: The spread between U.S. and Canadian 10-year government bond yields could impact portfolio allocation and currency-hedging decisions.

- Inflation Expectations: Breakeven inflation rates and (U.S.) Treasury Inflation-Protected Securities (TIPS) pricing might offer insight into the market’s read on central bank credibility and future policy moves.

- Bond Fund Flows: Monitor how institutional and retail investors reallocate between duration strategies and across fixed income exposures in response to policy shifts.

Possible Rate Scenarios

“With both the Fed and the BoC announcing their benchmark rate decisions on the same day, we have been seeing market participants position themselves ahead of expected rate cuts, driving an uptick in implied volatilities across markets,” Global X’s Daigle adds.

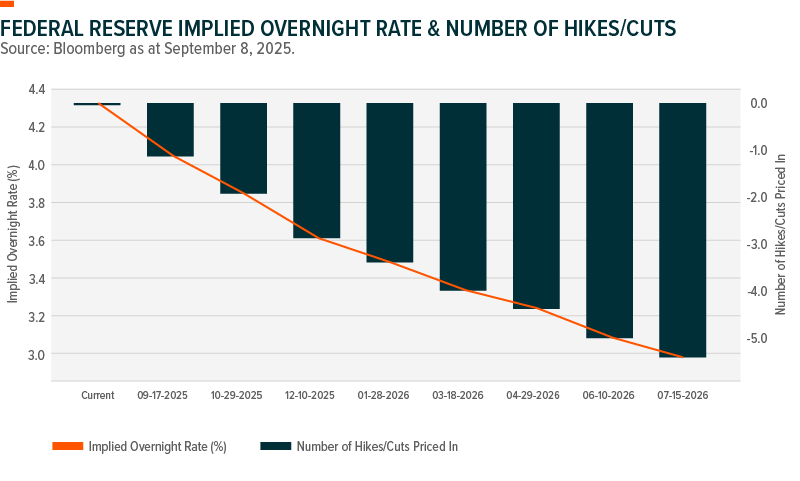

As of early September, markets are assigning a 90% probability of a BoC rate cut while for the Fed, they appear to be pricing in a 25-basis point (bps) cut, with the possibility of additional easing in the fourth quarter of the year.

Bloomberg’s World Interest Rate Probability (WIRP) is a forecast for central bank policy rates based on pricing from derivatives markets. It is seen as a gauge of investor assumptions on where interest rates may be headed. These are market predictions for where the BoC and Fed’s interest rate strategy could lead:

ETFs For a Changing Rate Reality

As the BoC and Fed begin potential easing cycles, Global X’s Premium Yield suite of exchange traded funds (ETFs) offers an innovative approach to income generation with ETFs such as Global X Short-Term Government Bond Premium Yield ETF (PAYS), which can provide a stable income alternative in today’s evolving market landscape. Additionally, for investors who may be looking to extend duration (and volatility profile) amidst a changing market environment, Global X Mid-Term Government Bond Premium Yield ETF (PAYM) would provide that increased duration for additional yield.

By combining traditional bond income with an options overlay, Global X’s Premium Yield suite offers enhanced yield potential, a degree of downside protection, reduced volatility and consistent cash flow.

The Premium Yield suite is designed for income-focused investors who prioritize enhanced yield over capital appreciation. For investors seeking tax efficiency, these ETFs provide an opportunity to enhance yield across different durations while maintaining exposure to North American government bonds.

With rate decisions looming, Canadian and U.S. central banks face diverging data and investor expectations. Easing cycles, yield curve shifts, and inflation outlooks are reshaping bond strategies—bringing defensive positioning, interest-rate sensitivity, and income-generation tools such as Global X’s Premium Yield ETFs back into focus for today’s complex macroeconomic environment.

Global X is due to launch two new ETFs based on 1-3 year and 20-year U.S. treasury bond indices. Further details will appear on the Global X website.

Related ETFs

PAYS – Global X Short-Term Government Bond Premium Yield ETF

SPAY – Global X Short-Term U.S. Treasury Premium Yield ETF

SPAY.U – Global X Short-Term U.S. Treasury Premium Yield ETF

PAYM – Global X Mid-Term Government Bond Premium Yield ETF

MPAY – Global X Mid-Term U.S. Treasury Premium Yield ETF

MPAY.U – Global X Mid-Term U.S. Treasury Premium Yield ETF

PAYL – Global X Long-Term Government Bond Premium Yield ETF

LPAY – Global X Long-Term U.S. Treasury Premium Yield ETF

LPAY.U – Global X Long-Term U.S. Treasury Premium Yield ETF

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The Global X money market funds are not covered by the Canada Deposit Insurance Corporation, the Federal Deposit Insurance Corporation, or any other government deposit insurer. There can be no assurances that the money market fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the Funds will be returned to you. Past performance may not be repeated. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2025 Global X Investments Canada Inc. All Rights Reserved.

Published September 15, 2025.

How Canadian Investors Use Finfluencers to Learn About Investing

Not ready to invest, but curious to learn more?

Subscribe for research perspectives, market commentary, and charts of the trends shaping global markets. We promise not to overwhelm you – updates will be periodic and timely.