Key Takeaways

- Canada’s equities have shown solid performance for the year to date. With 73% of TSX stocks in the green and nearly half delivering double-digit returns, performance for the year so far was strong, with financials, consumer staples and utilities making up 40% of the main TSX Composite index.

- Canadian sentiment is shifting toward homegrown exposure. Retailers like Canadian Tire reported surging sales, while nearly half of Canadians favour lowering pension fund holdings in U.S. assets, signaling a growing preference for domestic investment.

- U.S. equities show signs of concentration and uncertainty. The S&P 500® is weighted towards technology names, with Big Tech companies being seen as the primary drivers of U.S. equity performance as of late. Combined with waning growth forecasts and lingering tariff concerns, this narrow market could raise questions for diversified equity portfolios.

Canadian investors enjoy a strong 2025 – so far

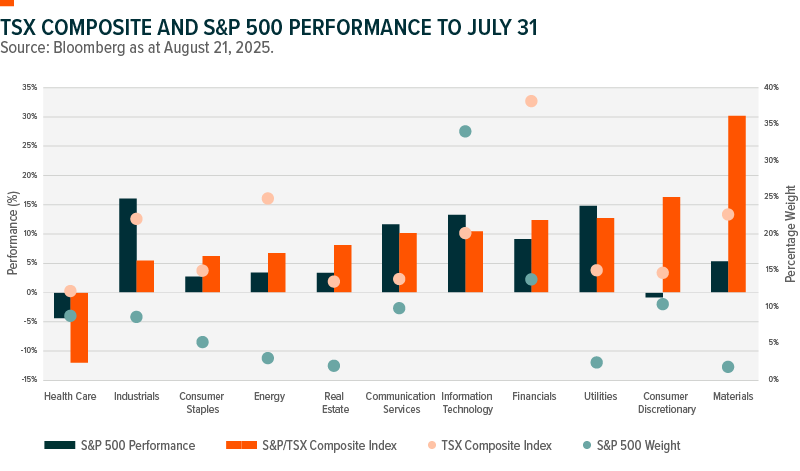

Despite tariff tensions, Canadians have enjoyed a strong 2025, so far, with the main equities market showing solid performance: from the start of the year to July 31, the S&P/TSX® Composite Index has gained 9.5%. South of the border, the S&P 500 advanced 6.8%.

As of the latest data1, 73% of the S&P/TSX Composite constituents are in positive territory, and nearly half have returned more than 10%.

In contrast, U.S. equities are posting more muted figures. So far this year, only 46% of the S&P 500 are up, and just 36% have delivered double-digit returns. The share of stocks outperforming the index stands at 39%, trailing historical norms.2

Part of a backlash to President Donald Trump’s trade war and annexation threats, has seen Canadian consumers boycotting or reducing their business with U.S. companies. Domestic retailers have used advertising and signs to wrap themselves in the maple leaf or make it easier for customers to find Canadian products on store shelves: Canadian Tire said retail sales jumped 6.4% at its eponymous big box stores during the second quarter of 2025.

Also, almost half of Canadians — 47% — believe that pension fund managers should be reducing their holdings of American assets, according to a poll conducted by Nanos Research for Bloomberg News.

Canada’s equity market continues to stand out for its defensive profile. Financials, consumer staples, and utilities account for 40% of the S&P/TSX Composite Index, underscoring its tilt toward high-dividend, lower-volatility sectors.

In contrast, the S&P 500® skews more aggressive. Defensive sectors represent a far smaller share, while technology driven by the “Magnificent Seven” makes up 35% of the index’s total weight.

American Exceptionalism Tamed?

This trend—fewer outperformers in a rising market—has persisted since the 2008 Global Financial Crisis and may reflect the increasing dominance of mega-cap and technology names in U.S. equity performance.

Uncertainty over U.S. tariffs is acting as a drag on global growth, with the OECD forecasting global growth slowing to 2.9% from 3.3% in both 2025 and 2026. The organization projects that the U.S. economy will slow from 2.8% growth in 2024 to 1.6% for the current year and 1.5% in 2026.

Current U.S. economic activity data has been softening but has yet to show signs of an official recession, whilst resilient consumer consumption and the passage of President Trump’s “Big Beautiful Bill” could benefit small- and medium-sized firms operating in sectors that will see increased spending coming from this piece of legislation.

A record 91% of fund managers now view U.S. equities as overvalued, following the sharp rebound off April lows—marking the highest reading in data going back to 2001.

Despite these concerns, broader sentiment has improved. Investor optimism reached its strongest level in six months, recovering from the market volatility sparked by President Trump’s latest round of tariffs.

“Despite a record number of fund managers calling U.S. stocks overvalued risk appetite has improved and U.S. equity overweight allocations have risen,” says Global X ETF Strategist Raghav Mehta.

“Professional fund managers have been less underweight U.S. equities into mid-summer versus the spring, hinting at a reluctant participation despite valuation worries.”

Currency Considerations

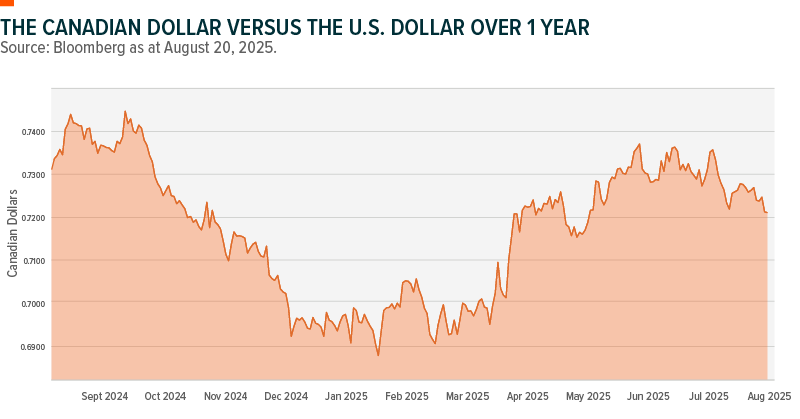

Despite erasing its 8% decline from 2024, the Canadian dollar has softened recently after a weaker-than-expected domestic inflation print and weakening labour market signals, while lower oil prices and risk sentiment shifts have augmented the moves in foreign exchange.

Markets have priced in the increasing probability of Bank of Canada (BoC) rate cuts, creating a near-term headwind for the loonie as the policy outlook narrows.

That said, CAD could still see modest appreciation if commodities stabilize or rebound and if Federal Reserve-BoC rate differentials compress over the medium term.

Timing is uncertain and volatility is likely. For Canadian investors, staying unhedged exposes U.S. equity returns to foreign exchange risks, i.e. a stronger loonie would detract from U.S. equity gains, while a weaker loonie may add to the upside. Remaining currency-hedged removes that volatility but it comes with explicit costs and could underperform in case the Canadian dollar weakens.

“CAD has been volatile; currency strategists are flagging a soft CAD versus USD year-to-date with mixed forecasts near-term. A firmer CAD would dampen US equity returns for unhedged Canadians; a weaker CAD boosts them,” Global X’s Raghav Mehta said.

Old Trade vs New Trade

For the near-term, Global X’s Mehta suggests a “barbell” approach when considering North American investments: “Tilt towards the U.S., diversify into Canada. Still lean into the U.S. for earnings leadership/Artificial Intelligence (AI), but many recommend adding to Canada based on attractive valuations, broadening breadth, and potential catch-up, especially if the price of oil stabilizes and rate cuts progress.”

Regarding the bullish investment case for the U.S., Mehta says he sees AI and Big Tech still delivering upward earnings revisions into 2026; even critics concede that the fundamentals are stronger than the early 2000s. In terms of U.S. risks, Mehta sees “crowded leadership and stretched multiples”.

For Mehta’s bullish investment case for Canada, he sees cheaper valuations, possible BoC rate cuts and an investment mix of financials/materials/energy tied to a global recovery narrative.

“Some Canadian houses argue TSX earnings growth can be similar to the S&P 500 in 2025, which challenges the valuation gap.”

As for Canada headwinds, the Global X’s ETF strategist sees smaller tech weighting, slower domestic growth versus the U.S. and oil price uncertainty (the IEA warns of oversupply into late-2025 and Goldman Sachs’s base case for Brent crude in the second the half of the year is for mid-US$60s).

Canadian equities are having a strong 2025, outpacing U.S. markets with broader gains. Yet, dispersion remains high and gold plays a key role in headline performance. Meanwhile, the Canadian dollar, trade tensions, and U.S. equity valuation concerns are prompting many investors to rethink regional allocations and currency-hedging strategies.

Related ETFs

CNDX – Global X S&P/TSX 60 Index ETF

CNCC – Global X S&P/TSX 60 Covered Call ETF

CANL – Global X Enhanced S&P/TSX 60 Index ETF

CNCL – Global X Enhanced S&P/TSX 60 Covered Call ETF

USSX/USSX.U* – Global X S&P 500 Index ETF

USCC/USCC.U* – Global X S&P 500 Covered Call ETF

USSL – Global X Enhanced S&P 500 Index ETF

USCL – Global X Enhanced S&P 500 Covered Call ETF

DLR/DLR.U* – Global X US Dollar Currency ETF

* Trades in U.S. dollars

Footnotes

1 Source: Scotiabank Global Banking and Markets ETF Edge note as at August 13, 2025.

2 Ibid.

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The Global X money market funds are not covered by the Canada Deposit Insurance Corporation, the Federal Deposit Insurance Corporation, or any other government deposit insurer. There can be no assurances that the money market fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the Funds will be returned to you. Past performance may not be repeated. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2025 Global X Investments Canada Inc. All Rights Reserved.

Published August 26, 2025.

How Canadian Investors Use Finfluencers to Learn About Investing

Not ready to invest, but curious to learn more?

Subscribe for research perspectives, market commentary, and charts of the trends shaping global markets. We promise not to overwhelm you – updates will be periodic and timely.